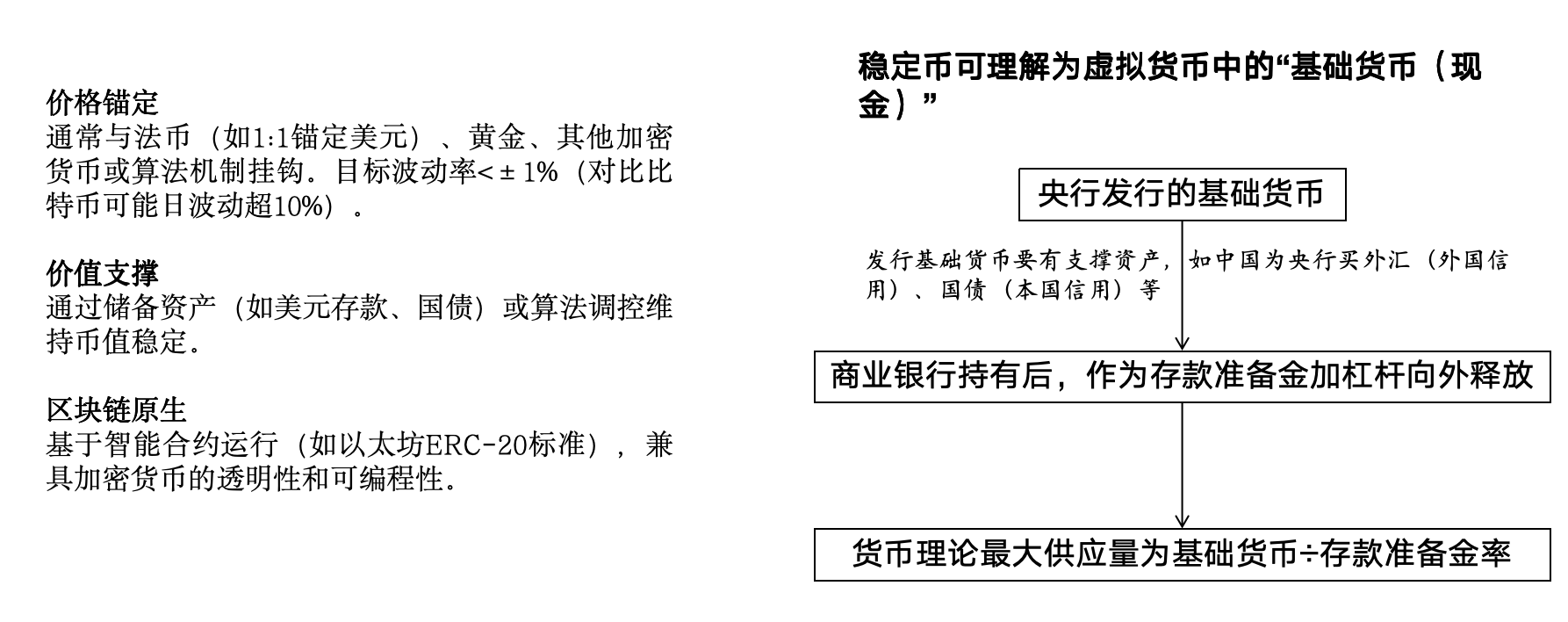

Stablecoin: It can be understood as the "base currency (cash)" (Bitcoin and other similar stocks) in virtual currency, which amplifies the amount of funds invested through bank loans and deposits (currency multiplier), and is the pricing unit of the virtual market. Issuance method: users deposit money equivalent to exchange for stablecoins - circulation of stablecoins between users - users hand over stablecoins to destroy to withdraw money. (similar to casino chips) Compared with the high efficiency of traditional currencies, the cost of cross-border transactions is extremely low, only about 10%; Compared with cryptocurrencies, it is more stable, with reserve assets as the underlying support, and the price volatility is small, which can be used as a risk hedging tool. Bridge between reality and virtuality: At present, the mainstream is an off-chain stablecoin, which is guaranteed by real world assets, such as US dollars, US bonds, euros and other assets, and is usually issued 1:1, which is a bridge between reality and virtuality. Competitive landscape: one super (USDT) and one strong (USDC) are blooming.

Overview of stablecoins

What is a stablecoin?

A stablecoin is a cryptocurrency that is backed by a specific asset and aims to maintain price stability. Its core design goal is to solve the problem of excessive price volatility of traditional cryptocurrencies (e.g., Bitcoin, Ethereum) and thus be more suitable as a medium of exchange, store of value, or unit of account.

Types of stablecoins

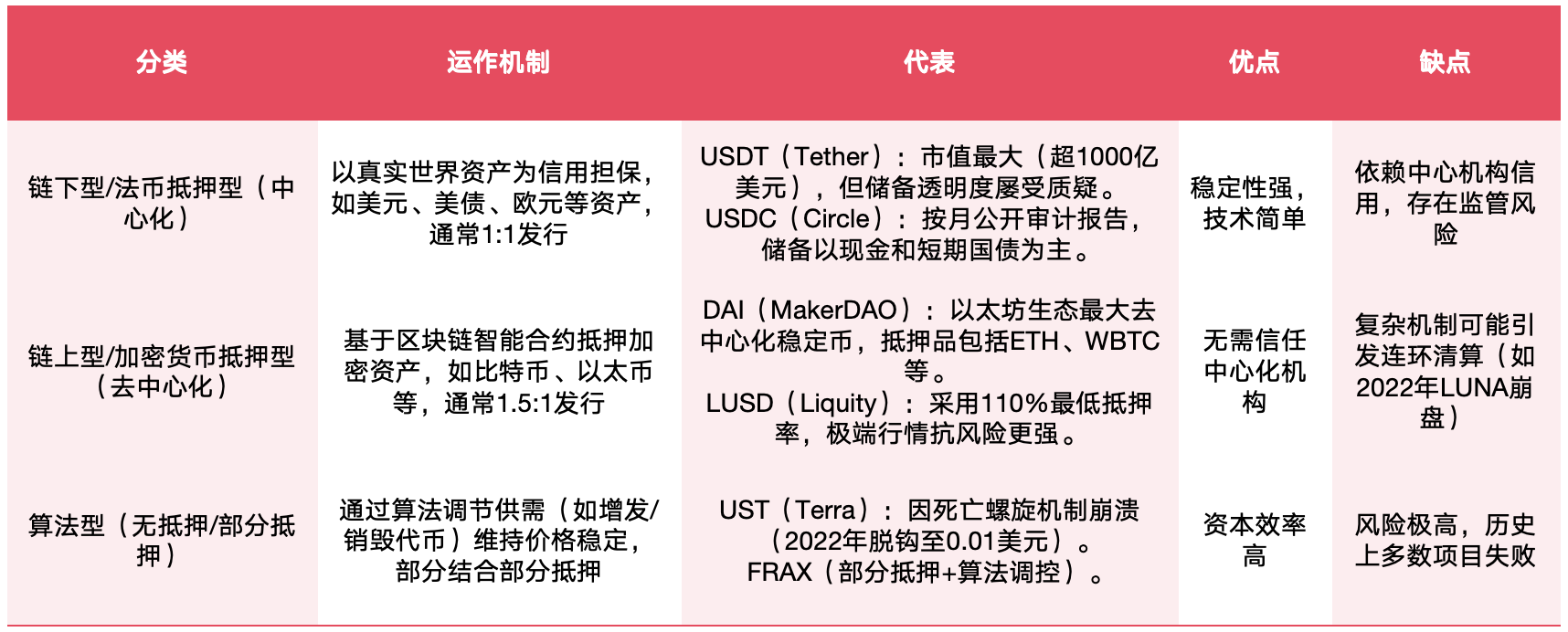

According to the different anchor objects and operating mechanisms, stablecoins can be divided into off-chain asset-backed stablecoins (Off-chain-backed Stablecoin), on-chain asset-backed stablecoins (on-chain-backed Stablecoins) and algorithmic Stablecoin)。

The core purpose of stablecoins

1. Crypto market trading medium: Compared with volatile virtual currencies (similar to stocks) such as Bitcoin, stablecoins are more like currencies recognized by the mainstream market. At present, stablecoins have accounted for more than 70% of the total trading volume of cryptocurrencies, avoiding frequent fiat currency deposits and withdrawals.

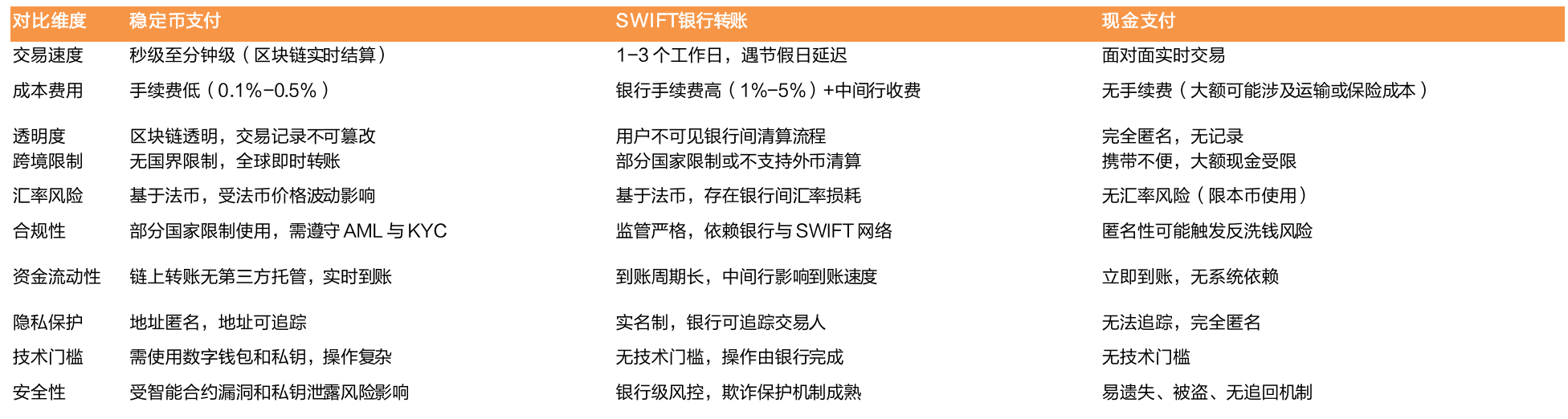

2. Cross-border payment and remittance: The traditional payment system is mature and extensive, but there are obvious drawbacks, such as high transaction costs (the average cost of cross-border transfer of $200 is 6.35%), long settlement cycle (especially on holidays or weekends), and lack of transparency. In contrast, stablecoins run on public blockchains, which typically have the advantages of lower cost (0.1%-0.5%), faster speed (seconds to minutes), and greater traceability.

3. DeFi infrastructure: as collateral for lending (such as USDT deposits in Aave with an annualized rate of about 3-5%), liquidity mining underlying assets.

4. Anti-inflation tools: People in high-inflation countries (such as Argentina) save through USDT to avoid the depreciation of their local currency.

5. Corporate financial tools: Tesla and other companies have accepted bitcoin payments and immediately converted them into stablecoins to hedge against volatility.

The development history of stablecoins

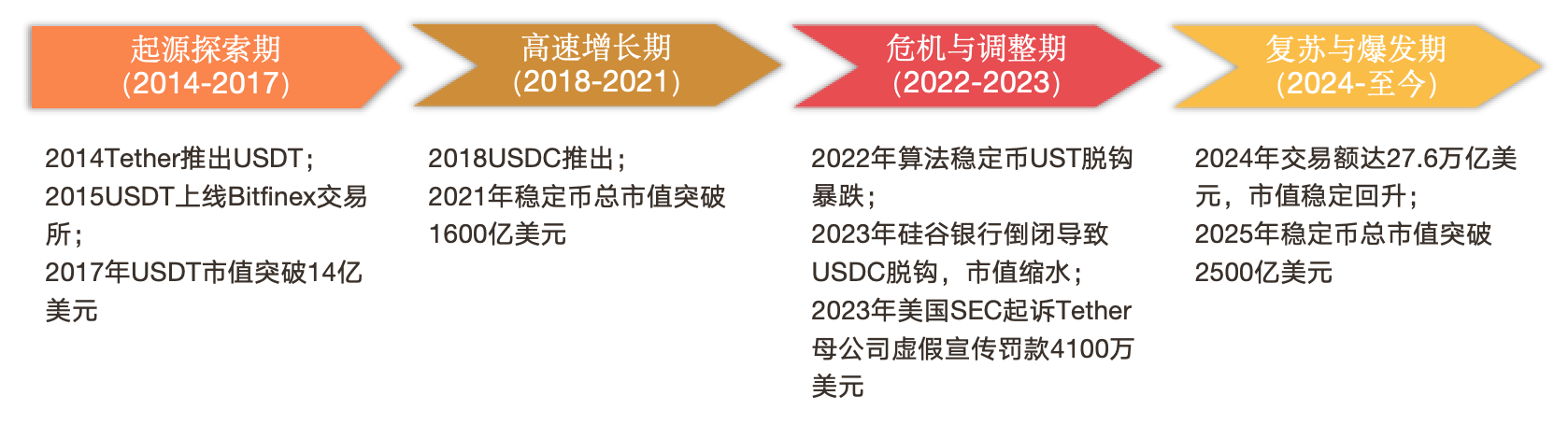

(1) Origin and exploration period (2014-2017): Tether launched the first stablecoin USDT, anchored to the US dollar 1:1, aiming to solve the problem of high volatility of cryptocurrencies and complex fiat currency exchanges, and become a "value bridge" for crypto transactions.

(2) High-growth period (2018-2021): In 2018, Circle and Coinbase launched USDC, winning wider trust with high transparency and compliance (monthly audit reports). Benefiting from the crypto bull market, exchange popularization, and safe-haven demand in emerging markets, the total market capitalization of stablecoins soared from $1.4 billion in 2017 to $163 billion at the end of 2021.

(3) Crisis and adjustment period (2022-2023): In May 2022, the depegging of algorithmic stablecoin TerraUSD (UST) plummeted, causing market panic, and the market value of USDT shrank to $65.8 billion, and USDC fell to $25 billion due to the collapse of Silicon Valley Bank.

(4) Recovery and outbreak period (2023-present): From the second half of 2023 onwards, transparency and regulatory improvements will drive market recovery. The total market capitalization will exceed $250 billion in 2025 (an 11-fold increase in five years), and the transaction volume will reach $27.6 trillion in 2024 (more than Visa and Master combined). The application is accelerated from crypto transactions to cross-border payments, DeFi, corporate settlements and other scenarios.

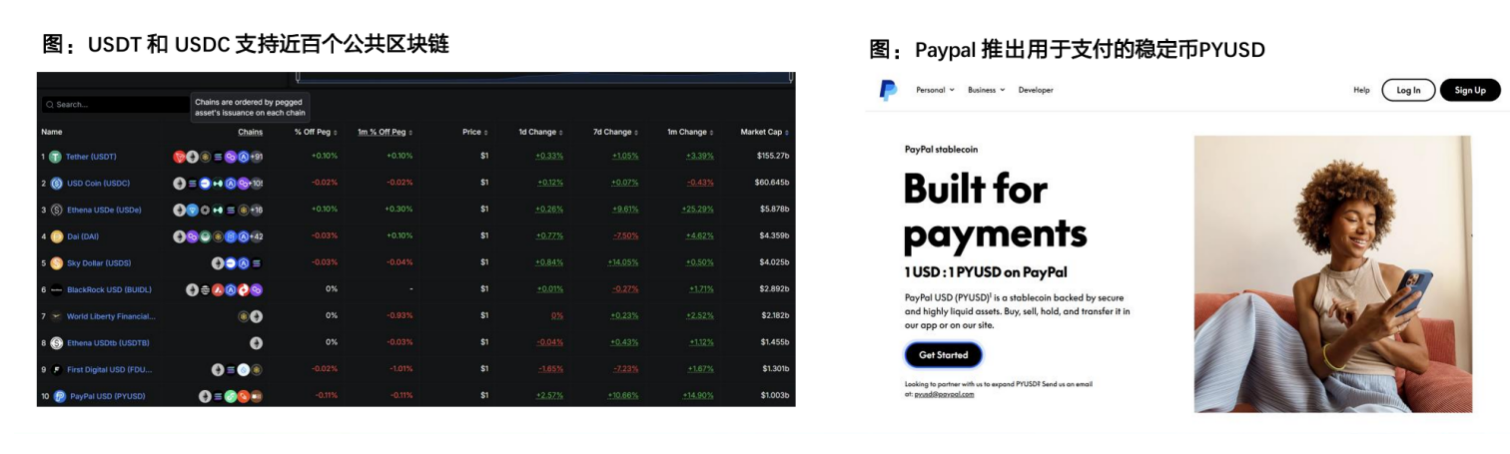

Competitive landscape: one super, one strong, a hundred flowers blooming

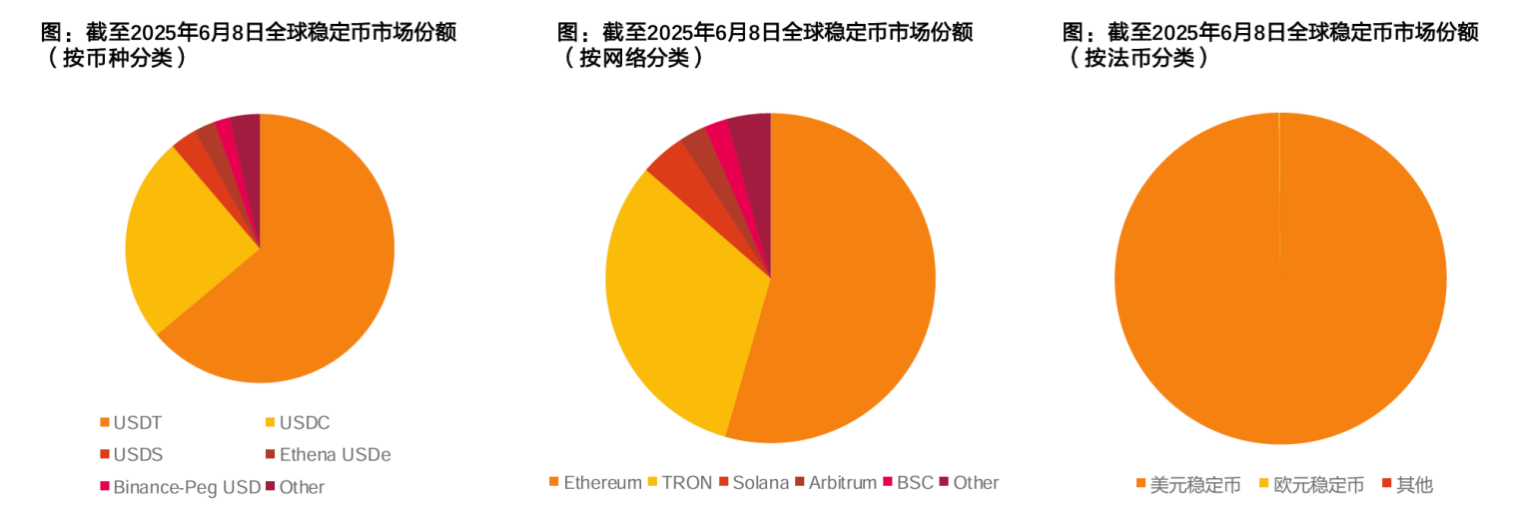

The stablecoin competitive landscape is highly concentrated, with USDT and USDC accounting for the majority of the market share by currency. According to rwa.xyz data, as of June 8, 2025, the world's top three stablecoins account for 92% of the market share, and the market capitalization of the top three stablecoins USDT, USDC and USDS is $151.1 billion/58.8 billion/$7.6 billion, with a market share of 64%/25%/3%, respectively.

By network, Ethereum is the main market for stablecoin circulation and USDC circulation. According to rwa.xyz data, as of June 8, 2025, about $129.1 billion of stablecoins were issued in Ethereum, accounting for 54% of all stablecoin issuance. The highest share of stablecoins on Ethereum is USDT with 54%, followed by USDC with 30%.

Ethereum is the largest public chain in circulation in USDC, with about 39.3 billion UDSC in Ethereum, accounting for 67% of the total market capitalization of USDC. TRON is the largest public chain in circulation of USDT, with about 74.7 billion USDT in TRON, accounting for 49% of the total market value of USDT.

By peg fiat currency classification, USD stablecoins account for almost all of the market share. According to rwa.xyz data, as of June 8, 2025, the market share of the US dollar stablecoin is 99.8%, and the market share of the second-ranked euro stablecoin is only 0.2%.

Competitive landscape: traditional financial institutions and governments have entered the market

In the context of the rapid development of the stablecoin market and the increasingly clear regulation, traditional financial institutions and governments have successively launched stablecoin products.

PayPal: Launched in 2023 the stablecoin PYUSD, which is fully collateralized by US dollar deposits, short-term US Treasury bonds and cash equivalents for payment scenarios. Robinhood: 2024 with Galaxy Digital, Kraken, Nuvei, and Paxos have partnered to launch the stablecoin USDG. Wyoming, USA: In March 2025, it tested its self-developed stablecoin WYST on multiple blockchain platforms. Fidelity Investments: In March 2025, its digital asset division was testing a stablecoin. The Trump family: In March 2025, the Defi project World is supported Liberty Financial launches USD1, a stablecoin pegged to the U.S. dollar.

At present, the main market share of stablecoins is occupied by USDT and USDC, with obvious first-mover advantages, and currently supports nearly 100 public chains, and the competition caused by latecomers is relatively limited.