Circle: The first share of stablecoin, the product is mainly USDC, which has the following differences compared with USDT: Business model: USDT money printing machine model, as long as you exchange money, you will take a commission; USDC narrow banking model, the main income is the stored value interest income of the money exchanged; Core features: USDT has a high proportion of gray market, USDC is more compliant, has obtained compliance licenses from multiple countries, and reserve assets are more adequate and transparent. Main challenges: The revenue is too simple, and it currently relies on the channel Coinbase to take 60% of the revenue, and there are challenges in the business model.

Circle

Build the world's largest compliant stablecoin network with USDC as the core

Founded in 2013 by Jeremy Allaire and Sean Neville, Circle aims to build a new financial architecture based on open networks, software, and global connectivity. USDC, issued by Circle in 2018, is currently one of the most widely used compliant payment stablecoins in the world.

USDC issuance, circulation and destruction mode: The USDC model is basically the same as USDT, which is mainly divided into five steps: first, users deposit US dollars into Circle's bank account; Second, Circle mints the equivalent value of USDC in the user's account; third, it is the circulation between users; Fourth, redemption, if the user redeems the USD, they need to hand over the USDC to the Circle company; Fifth, Circle burns USDC while returning the equivalent value of USD to the user's bank account.

The difference is that USDC minting is only used by exchanges, institutional traders, wallet providers, banks, and large financial institutions, and the minting is free, and individuals cannot apply to mint USDC. USDT, on the other hand, can be minted as long as it reaches $100,000, and there is a fee.

|商业模式:主要依赖储备收入,商业模式更稳健

USDT的商业模式(印钞机):Tether公司的盈利主要来源于两方面,首先是出入金手续费和注册KYC后的服务费,Tether公司只接受10万美元以上的赎回或者铸造USDT,每次铸造USDT的费率为0.1%,赎回费用为(0.1%或者1000美元的较高者),验证费为150美元/人。其次是投资收益,Tether公司用储备金进行资产配置的资金也构成了Tether的收入。据深潮TechFlow,2024年Tether年利润达到130 亿美元。

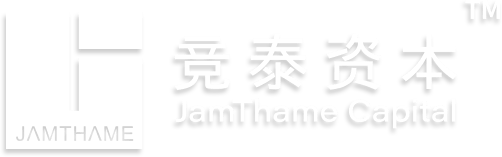

USDC's business model (narrow bank): USDC's business model is also similar to USDT, the difference is that the USDC minting process is free, and 81.49% of the assets held by USDT are invested in cash and cash equivalents and other short-term deposits, while USDC is close to 100%, so the yield on the asset side will be lower. In 2024, Circle will achieve revenue of $1.68 billion and net profit of $156 million, which is quite different from USDT.

Revenue grew steadily, with profit declining last year due to distribution agreements

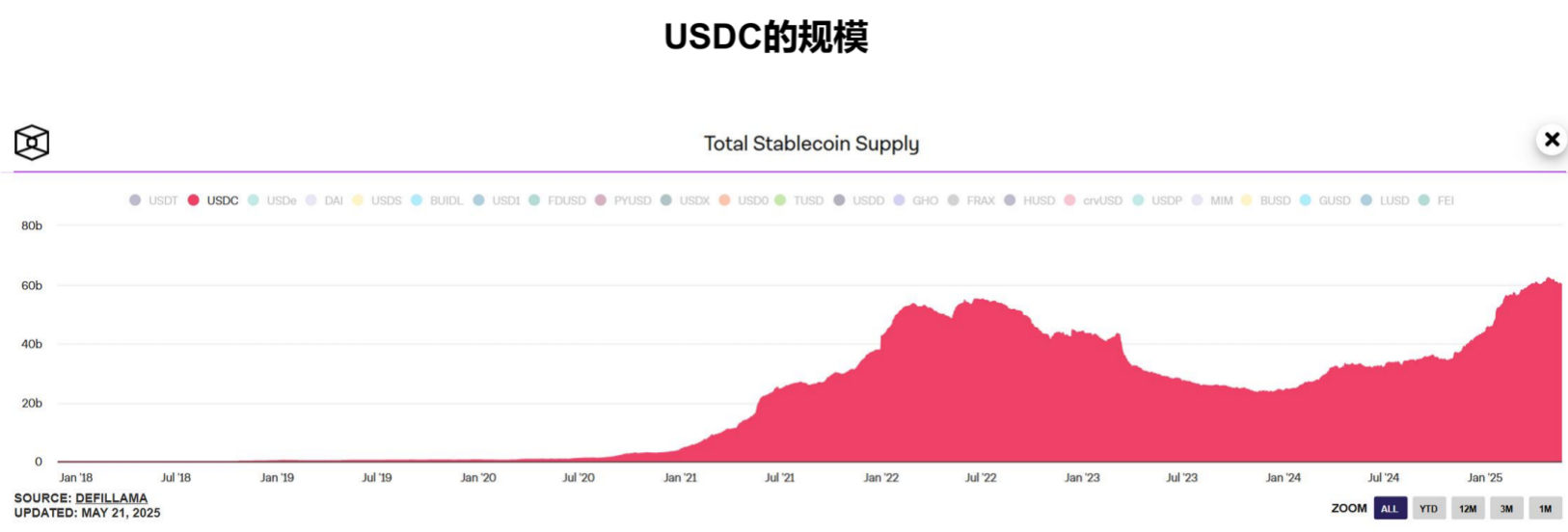

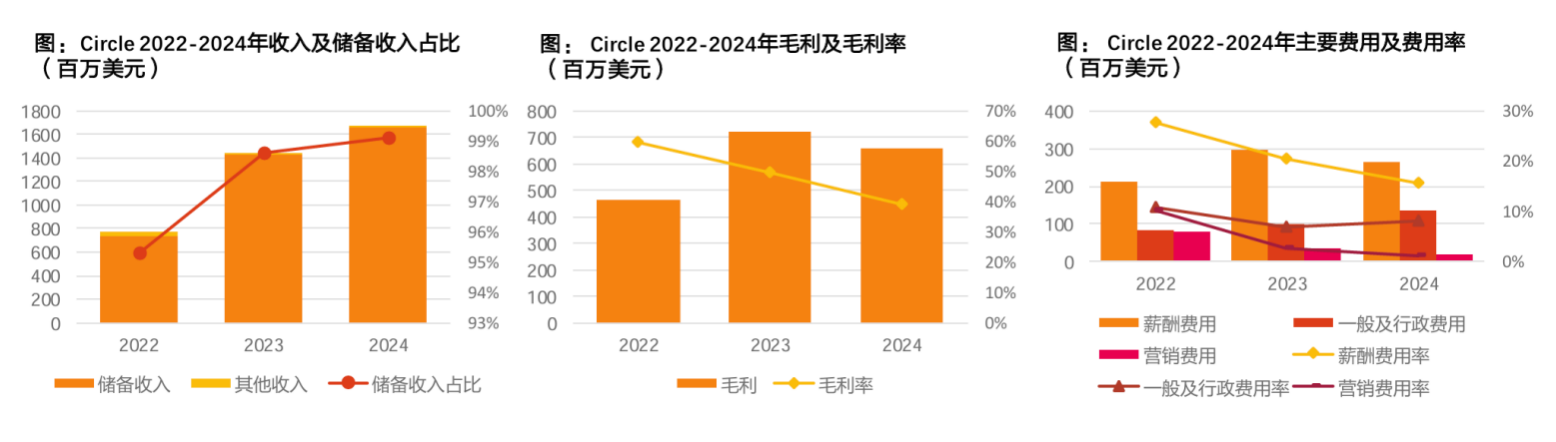

Revenue: From 2022 to 2024, the total revenue will be 770 million/1.45 billion/$1.68 billion, of which reserve income will account for 95%/99%/99% respectively, and the company's revenue growth will be mainly driven by interest income from USDC reserves.

Gross Profit: Circle does not disclose gross margin in the traditional sense, and its gross profit is calculated as revenue minus distribution, transactional, and other costs. From 2022 to 2024, the gross profit margin will be 60%/50%/39% respectively, and the decrease in gross profit is mainly due to the change in the sharing ratio of Circle and Coinbase signed a branch cooperation agreement with Coinbase in August 2023.

Expenses: Operating expenses from 2022 to 2024 will be 500 million/450 million/490 million US dollars, respectively, and the operating expense ratio will continue to decline under the scale effect brought by revenue and gross profit growth, which will be 65%/31%/29%, respectively.

Profit: The company turned losses into profits in 2023 and declined in 2024 due to the impact of distribution agreements on gross margins. The company's net profit from 2022 to 2024 will be -770 million/270 million/160 million US dollars, respectively.

Core Strengths: Infrastructure, ecosystem, and compliance paths build core competitiveness

Circle has a well-established infrastructure for the internet financial system. The Circle stablecoin network consists of four business pillars, namely the Circle stablecoin, the Circle tokenization fund, the Circle liquidity service, and the Circle developer service.

Circle partners with leading ToC companies and applications to expand the reach, scale, utility and value of the network. Circle partners include digital asset exchanges (e.g., Coinbase, Binance), digital banks, brokerages (e.g., Robinhood), payment service providers (Block), remittance services (e.g., MoneyGram), super app platforms (e.g., Grab), and e-commerce companies (e.g., MercadoLibre).

Circle continues to expand its business licensing in global markets, with a focus on compliance and security. Circle has been licensed to operate stablecoin businesses in the United States, Singapore, Bermuda, the United Kingdom, and the European Economic Area (EEA), and is exploring applying for licenses in additional markets to support the minting of Circle stablecoins in these regions and provide underlying market liquidity. Circle's reserve assets are regularly audited by the Big Four accounting firms to enhance transparency and credibility.

Challenges and Risks

Circle's core competitiveness lies in turning compliance into an ecological barrier, but its long-term value depends on whether it can break through the "narrow bank" model and become the core protocol layer connecting traditional finance and the crypto economy.

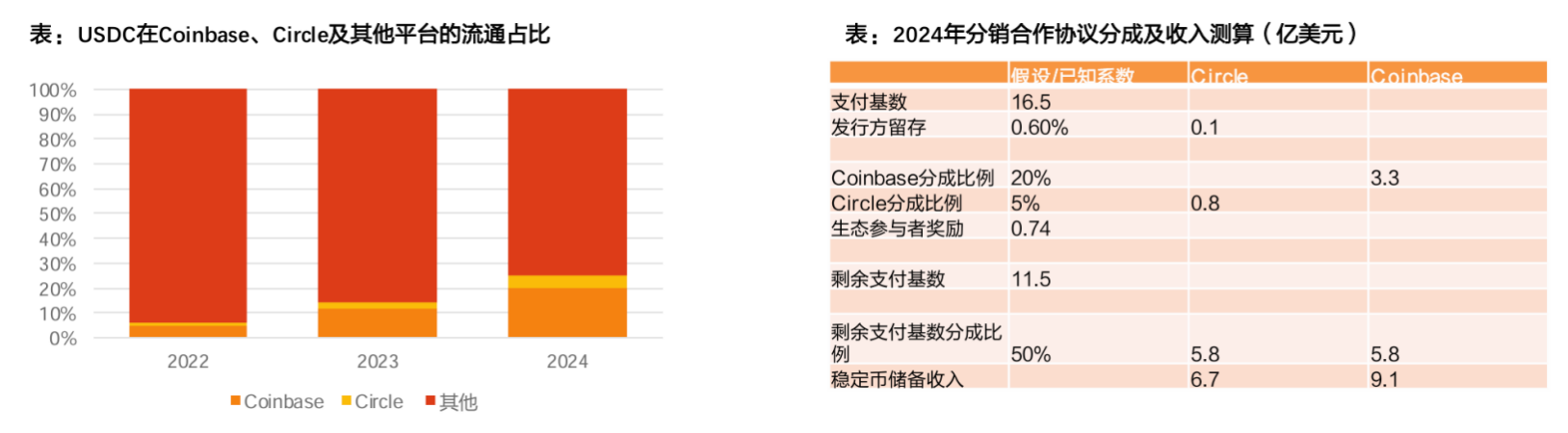

Income unity: 99% of profits depend on U.S. Treasury interest, and if the Fed cuts interest rates, income could shrink by 20%. Channel dependency: Coinbase takes 60% of its revenue ($908 million in 2024) and has limited bargaining power. Traditional financial competition: PayPal, JPMorgan Chase and other self-developed stablecoins may squeeze USDC's compliance scenarios. Policy uncertainty: The GENIUS Act in the United States may further tighten stablecoin regulations, and Circle's operating costs will rise if it requires higher capital reserves or restricts its business scope.

Hong Kong's Stablecoin Ordinance

Hong Kong, China: Actively legislating to establish a Hong Kong stablecoin

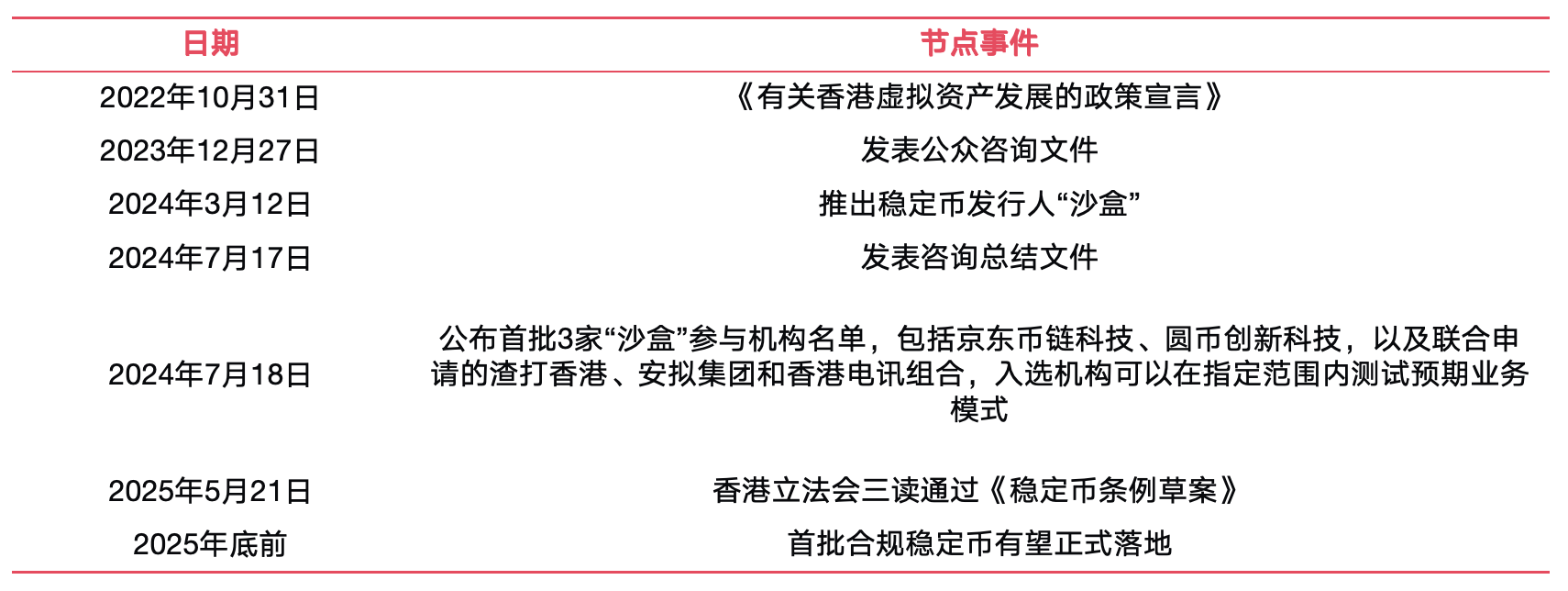

As an international financial center, Hong Kong's local government and regulators have been paying close attention to digital crypto assets. In 2022, the "About Hong Kong Virtual Assets" was released

Policy Statement on Development", followed by the publication of public consultation papers in this area, and the launch of a "sandbox" for stablecoin issuers to test related businesses. Finally, the Stablecoin Bill was passed on 21 May 2025 and published in the Gazette on 30 May 2025, officially becoming law, marking a new step in the regulation of virtual assets by the Hong Kong authorities.

Interpretation of Hong Kong Stablecoin Ordinance

Hong Kong's Stablecoin Ordinance is the world's first specific legislation for fiat currency stablecoin issuance: it marks Hong Kong as one of the first jurisdictions in the world to implement a dedicated regulatory framework for stablecoins (in addition to the United States, the European Union, Singapore, the United Arab Emirates, etc.). This legislation, which took only five months from draft to pass, represents Hong Kong's determination to maintain its status as an international financial center and accelerate its entry into the global virtual asset market. This legislation also promotes Hong Kong to become an international Web3 and digital financial center, laying the foundation for the internationalization of the renminbi and the launch of the renminbi stablecoin.

Hong Kong's Stablecoin Ordinance establishes the world's first full-chain regulatory system for fiat currency stablecoins, the key points of which are as follows:

• Define stablecoin activity:

(1) Clarify the meaning of stablecoins, central bank digital currencies, digital forms of securities and futures contracts (security tokens) are not stablecoins.

(2) All types of stablecoins issued in Hong Kong and stablecoins pegged to Hong Kong dollars issued worldwide are within the scope of regulation.

• Licensing system and entry threshold:

(1) Businesses related to both the issuance and stablecoin activities (e.g., payment and settlement) are required to obtain a license issued by the HKMA in advance.

(2) Only institutional entities can apply and need to meet the minimum capital requirements, and the actual controller and senior management are subject to penetrating supervision, which is subject to the approval of the financial administrator and the qualification and ability test.

•Licensee Entity Responsibility:

(1) The issuer must have sufficient or excess reserve assets, and the reserve assets are segregated and independently managed.

(2) The licensee shall meet a series of operational requirements, in particular a sound anti-money laundering, risk management, liquidity system and information disclosure system.

• Other important points:

(1) The licensee shall not pay interest on the issued stablecoins.

(2) If there are signs of bankruptcy or non-compliance of the licensed entity, the HKMA can take over directly, and the holders of stablecoins have the priority of liquidation.

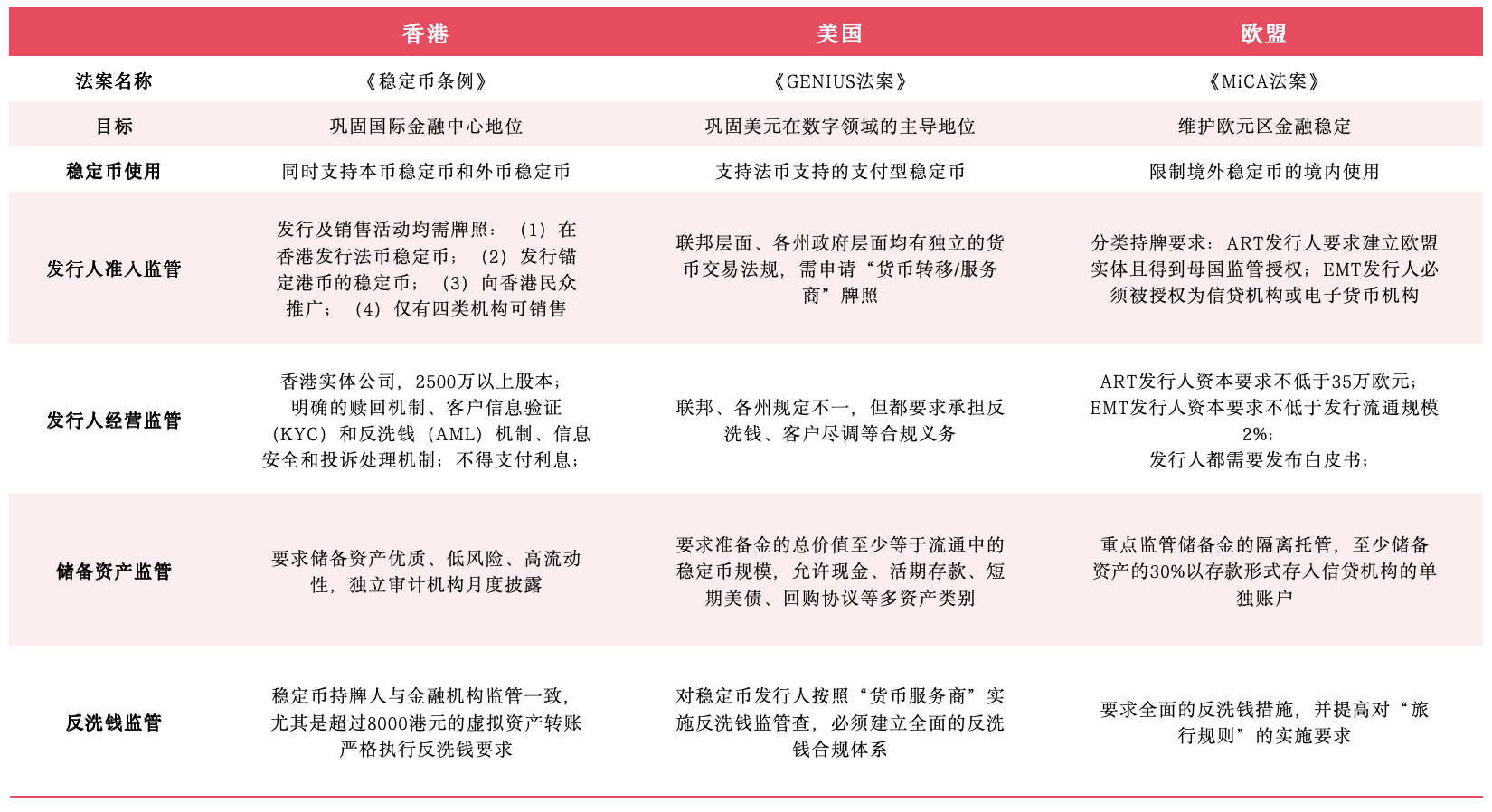

Comparison of regulatory acts in various countries