Recently, Buffett's Berkshire Hathaway disclosed its latest second-quarter position report on U.S. stock holdings, and the market's concern about Apple's reduction and "mysterious position" were finally exposed.

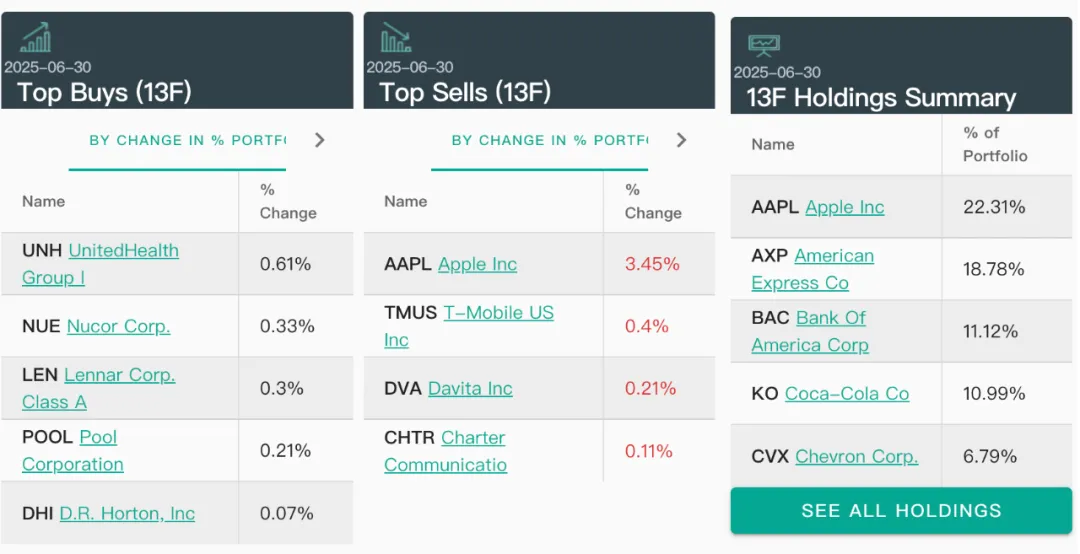

Berkshire reduced its holdings of Apple (AAPL) by 20 million shares in the second quarter, a decrease of 6.67% from the first quarter, and the proportion of Apple's holdings fell from 25.76% in the first quarter to 22.31%, and the market value of its holdings decreased by $4.1 billion.

Berkshire reduced its holdings in Apple and Bank of America and bought six new stocks, including: UnitedHealth Health, Newcor Steel, Reiner Construction, Holden House and Lamar Outdoor Advertising, and Ann Langer. Related new positions rose significantly after hours, with United Health and Nuke Steel rising more than 8% at one point.

|Reduction continues, but it is still the "number one heavy position"

This is the first time in half a year that Berkshire has disclosed a reduction in its holdings of Apple. In the second and third quarters of last year, Berkshire successively reduced its holdings of Apple, by 50% and 25% respectively, and since then, in the fourth quarter of last year and the first quarter of this year, Berkshire's Apple holdings have remained unchanged.

Regardless of the proportion of positions or changes in market capitalization, Apple was Berkshire's largest stock in the second quarter. Despite this, by the end of the second quarter, Berkshire still held about 280 million shares of Apple, and Apple was still the number one stock.

Another stock that Berkshire significantly reduced its holdings in the second quarter was Bank of America (BAC), which reduced its holdings by about 26.31 million shares in the quarter, down 4.71% month-on-month, and the market value of its holdings decreased by $1.24 billion, but the proportion of holdings rose slightly to 11.12% from 10.19% in the first quarter, still the third largest heavy stock.

Berkshire has reduced its holdings of Bank of America by more than 40% in the past year. By the second quarter of this year, Berkshire's Bank of America holdings had fallen from 1.03 billion shares in the middle of last year to 605 million shares, a drop of nearly 41.3%.

Berkshire liquidated 3.88 million shares of T-Mobile (TMUS) in the second quarter, and 0.4% of its holdings in the first quarter returned to zero, making the telecommunications giant second only to Apple in terms of Berkshire's holdings in the second quarter.

This is not a "panic selling", but a rhythmic "cash reserve + structural adjustment". Why do this? There are three possible reasons:

Lock in profits: Apple's stock price has been high for a long time, and some of the gains have been reduced to cash;

Dealing with uncertainty: the economic outlook is uncertain, and it is safer to hold cash;

Prepare for the "next big deal": Buffett often said that "bullets should be kept to hit the elephant".

Buffett's "mysterious positioning" has finally been revealed

The suspense of "mysterious positioning" left by Berkshire in the first quarter was revealed in the position report in the second quarter.

The company's second quarterly report did not disclose in detail small-scale investments other than heavy stocks such as Apple, but divided stock investments into three categories: financial, consumer goods and "commercial, industrial and others". As of the end of the second quarter, the targets of six new positions finally surfaced, including medical, steel, real estate and other targets, with a total market value of about US$3.65 billion at the end of the quarter. Although it is not the rumored 5 billion, the lineup is quite particular:

These purchases are completed gradually across quarters, so there are traces of "hiding" in the first quarter financial report, but the position report is not reflected. This is exactly Buffett's usual strategy: quietly open positions to avoid driving up costs.

Don't look at it as six stocks, in fact, the logic is very clear:

Medical (UNH): rigid demand, anti-cyclical;

Real estate (LEN, DHI): U.S. housing shortage, long-term mismatch between supply and demand;

Steel (NUE): beneficiaries of infrastructure and manufacturing reshoring;

These industries do not rely on technology outlets, but "live on solid cash flow".

Chevron was the only lucky person to be "increased" by Buffett in the second quarter

Among Berkshire's top ten heavy stocks, Chevron (CVX) was the only stock to increase its holdings in the second quarter. It increased its holdings by 3.45 million shares during the quarter, increasing its market capitalization by $495 million. But interestingly, despite buying more, Chevron's share of Berkshire's overall holdings fell from 7.69% to 6.79%.

Why is this? Don't worry, let's look at it layer by layer.

First look at the facts, among Berkshire's top ten heavy stocks, only Chevron was increased in the second quarter, and the others were either reduced or passively changed, increasing their holdings by 3.45 million shares, with real money increasing by nearly $500 million. However, due to the decline in oil prices and the weakening of stock prices throughout the second quarter, Chevron's market value shrank, resulting in a passive decline in its weight in the total position.

These actions show that Buffett is "buying more and more". This is very much in line with his usual style: when others panic, he sees that the attractiveness of cash flow and dividends is increasing. You know, Chevron is not only an energy giant, but also a "cash cow" with high dividends, low valuation and strong cash flow, which perfectly fits Berkshire's investment philosophy of "likes geese that can lay eggs".

Although individual stocks have increased and decreased, on the whole, Berkshire's "core holdings" are still very stable. By the end of the second quarter, the top ten heavy stocks were still the "old ten", most of the rankings were consistent with the first quarter, Apple, Bank of America, American Express, Coca-Cola, and Chevron. These "old friends" still firmly occupy the core position.

This shows that Buffett's underlying logic has not changed - he still trusts these blue-chip companies with simple business, deep moats, and stable dividends. Even while reducing his holdings of Apple and Bank of America, he did not look for "new stories", but continued to increase his familiar territory.