The impact of US tariffs on European goods is being felt.

With the official entry into force of the "reciprocal tariffs" on August 7 and the fading of the "export grabbing" effect, the downward trend of European exports to the United States is expected to accelerate. Deutsche Bank warned in the report that the decline observed so far is still milder than the model predicts, and that more severe shocks are yet to come.

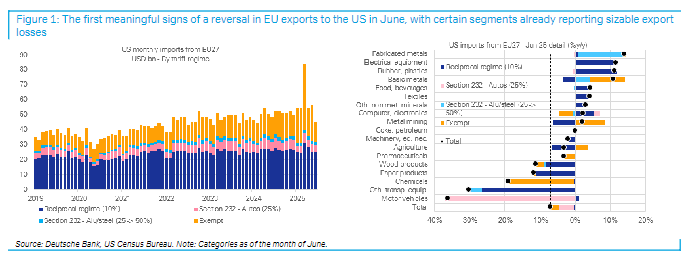

The "boomerang" of the United States imposing tariffs is smashing into European exports

The latest data shows that Europe's automobile exports to the United States plummeted 36% year-on-year in June, becoming the hardest hurt industry in this round of tariff war. This is not a small fluctuation, but a "cliff-like" decline.

The worst is undoubtedly the European automotive industry. automobile exports to the United States plummeted by 36% year-on-year in June; Germany, Italy, Sweden and other high-end car companies have shrunk sharply; The reason is straightforward, the United States has included European electric vehicles and some traditional fuel vehicles in the scope of tax increases, and the tariff on some models has been increased to 25%.

As a result, prices rose, orders were gone, and factories began to cut production. This is not only a trade friction, but also a precise blow to the "heart" of high-end manufacturing in Europe.

The car fell, and the person next to it was not spared. exports of other transportation equipment (such as trucks, buses, and special vehicles) decreased by 30%; Chemical exports fell by 19%, especially in categories that are highly dependent on the United States, such as fine chemicals and industrial additives. This shows that the "killing radius" of tariffs is expanding, no longer limited to a certain type of product, but forming a chain reaction at the industrial chain level.

Industries that are "strong" on the surface are actually bleeding. For example, the export data of base metals (steel, aluminum) and agricultural products (dairy products, alcohol) do not fluctuate much, but the truth is not that simple. The report pointed out that their "resilience" mainly comes from the fact that most products are exempt from tariffs. But note that those included in the "reciprocal tariff" list also saw a significant decline in exports to the United States by 7% to 18% during the same period!

As long as it is labeled as "taxed", no industry can really bear it. The so-called "stability" is just "survivor bias".

Another key factor affecting the June data is the "normalization" of drug exports. In March, due to market expectations of tax hikes in April, European pharmaceutical companies concentrated on exports; As a result, drug exports to the United States increased abnormally highly; In June, the demand released in advance "ebbed", and exports naturally fell sharply.

The report clearly pointed out that three-quarters of the overall export decline in June came from the "technical correction" of such tariff-exempt goods. This is like a period of exhaustion after an "export overdraft", not a real shrinking demand, but the data looks ugly.

The real storm hasn't come yet

The impact of this round of US tariffs has just begun to ferment. Let's start with a set of key data: in June, the average tariff on U.S. exports to Europe was 12%; Since August 1, this number has jumped to 16%. Don't underestimate the rise of these 4 percentage points, it means that corporate profits have been further squeezed, consumer prices have continued to rise, and order loss has accelerated.

More importantly, the current general tariff level of 15% is a full 50% higher than the 10% of the "moratorium" period from April to July! Deutsche Bank bluntly said that this tax rate is more "destructive", not "affecting a little", but may change the long-term flow of trade.

Some data looks "pretty good", such as: processed metal products, electrical equipment, rubber/plastic products. The export value of these categories is still increasing year-on-year and does not seem to have been affected much. But the truth is that they just "haven't reacted yet." It's like when you hit the brakes, the car doesn't stop immediately. The same is true for exports, with lag effects in order execution, inventory digestion, and contract performance.

Deutsche Bank's judgment is clear, if these industries are really not affected, it means that they are "grabbing US market share". But the reality is that the local production capacity of the United States is being protected, so how can Europe be so easy to grab? So, this growth is "strange", more like calm before a storm, and adjustments will come sooner or later.

The decline in exports in June was only a "preliminary impact", and the current data is still "relatively modest" compared to the overall losses that tariffs may bring. In other words: the most painful moment is yet to come.

How to deal with this "tariff storm"?

In the face of this "stress test" of the global supply chain, Jingtai's suggestion is:

Avoid European export-oriented industries that are highly dependent on the United States, especially automobiles, high-end machinery, fine chemicals, etc.; Even if short-term valuations are low, we must be wary of long-term suppression caused by policy risks.

Paying attention to local substitution and domestic demand opportunities in Europe, tariffs force Europe to accelerate "localized production"; For example: batteries, semiconductors, key raw materials; Domestic consumption and infrastructure investment may become new support.

Lay out supply chain restructuring enterprises that have "detoured to the sea", those European companies that have set up factories in Mexico, Eastern Europe, and Southeast Asia; Tariffs can be avoided through "third-country assembly" and export capacity to the United States can be maintained.